How your reimbursement settings change the final bill

What Does Pet Insurance Cover Guide to Benefits Exclusions and Limits

Content

Pet insurance can save you thousands of dollars when your dog needs emergency surgery or your cat develops diabetes. But the devil lives in the details—not all policies cover the same treatments, and many pet owners discover critical gaps only when filing their first claim.

Understanding exactly what your policy covers before you need it prevents financial surprises and helps you choose a plan that actually protects your pet. Most policies follow a similar structure, but variations in coverage, exclusions, and reimbursement terms can dramatically affect what you pay out-of-pocket.

Core Medical Treatments Covered by Most Pet Insurance Plans

Standard pet insurance policies focus on unexpected accidents and illnesses—the expensive, unpredictable events that can drain your savings overnight. These plans typically cover diagnostic tests, treatments, surgeries, hospitalization, and prescription medications related to covered conditions.

Accident coverage kicks in when your pet gets injured. If your dog breaks a leg chasing a squirrel, tears their ACL playing fetch, or eats something toxic, accident coverage handles the emergency visit, X-rays, surgery, anesthesia, pain medication, and follow-up care. Most policies cover accidents after a short waiting period of 2-3 days.

Illness coverage addresses diseases and health conditions that develop after your policy's effective date. This includes infections, cancer, diabetes, kidney disease, allergies, gastrointestinal issues, and respiratory problems. Illness waiting periods typically last 14 days, though some conditions like hip dysplasia may require 6-12 months before coverage begins.

When your vet suspects cancer, typical pet insurance coverage includes the diagnostic workup: bloodwork, urinalysis, X-rays, ultrasounds, CT scans, MRIs, and biopsies. If cancer is confirmed, covered treatments pets insurance policies usually pay for chemotherapy, radiation therapy, surgery to remove tumors, and medications to manage side effects. A full course of chemotherapy can cost $3,000-$10,000, making this coverage particularly valuable.

Hospitalization expenses add up quickly. An overnight stay at an emergency veterinary hospital easily runs $1,000-$3,000 per night when you factor in monitoring, IV fluids, medications, and nursing care. Most policies cover these costs as long as the underlying condition isn't excluded.

Prescription medications for covered conditions receive reimbursement under most plans. If your dog develops a bacterial infection requiring antibiotics, or your cat needs thyroid medication for hyperthyroidism, you'll submit the prescription costs with your claim. Medications for chronic conditions remain covered as long as the condition first appeared and was diagnosed after your coverage began.

Author: Ashley Reynolds;

Source: lamadone.net

Routine and Preventive Care: What's Typically Excluded (and How to Get It Covered)

Here's where confusion runs rampant: standard pet insurance policies exclude wellness and preventive care. Annual checkups, vaccinations, flea and tick prevention, heartworm testing, routine dental cleanings, and spay/neuter procedures don't qualify for reimbursement under basic accident and illness plans.

Insurance companies exclude these services because they're predictable expenses, not unexpected ones. You know your puppy needs vaccines and your adult cat requires annual bloodwork. Insurance is designed to protect against financial catastrophes, not routine maintenance costs.

That said, many insurers offer wellness riders or preventive care add-ons for an additional monthly fee of $10-$25. These packages provide a fixed annual allowance—typically $150-$500—that reimburses you for covered services pet insurance wellness plans include:

- Annual or biannual wellness exams

- Core and non-core vaccinations

- Heartworm, fecal, and other screening tests

- Routine bloodwork and urinalysis

- Flea, tick, and heartworm prevention

- Routine dental cleanings (without extractions)

- Nail trims and anal gland expression

Run the math before adding wellness coverage. If your annual preventive care costs $300 and the rider costs $240 per year, you're only saving $60. Some pet owners prefer setting aside that money in a dedicated savings account instead.

Author: Ashley Reynolds;

Source: lamadone.net

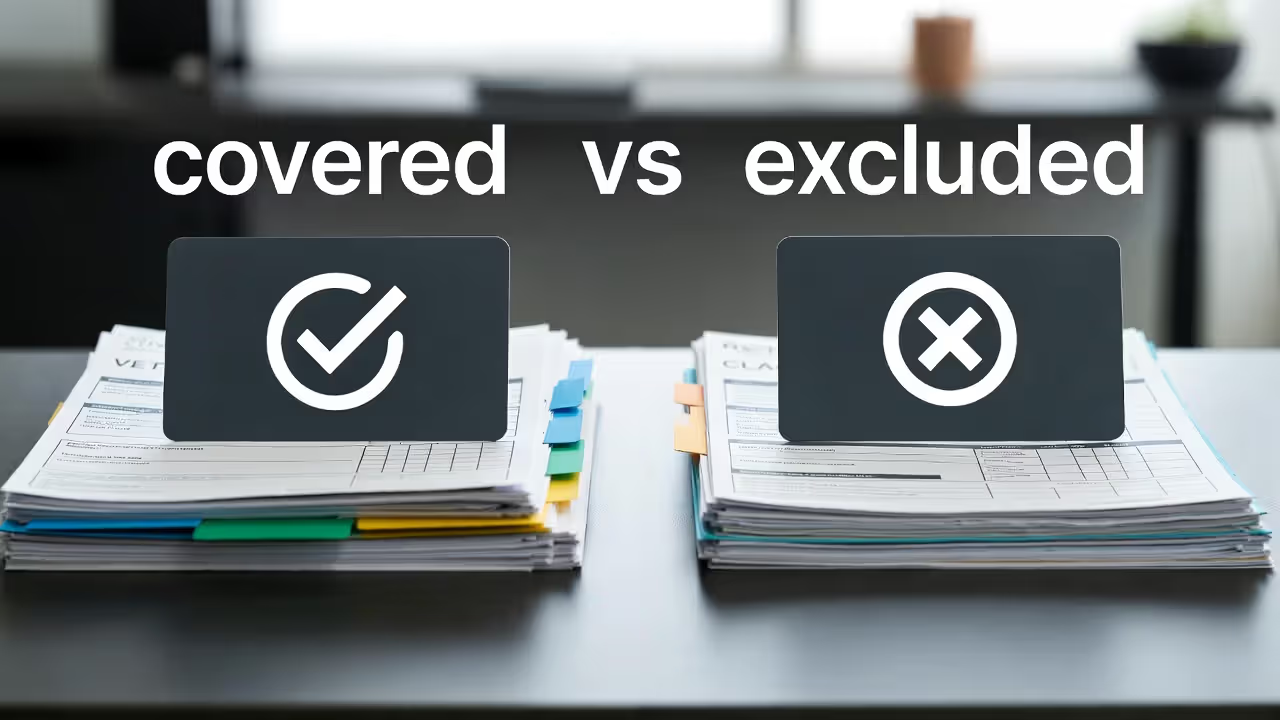

Common Vet Procedures and Their Insurance Coverage Status

Pet owners frequently ask about specific procedures when shopping for coverage. The answer often depends on why your pet needs the procedure—the same treatment might be covered in one scenario but excluded in another.

Take dental work as an example. If your dog fractures a tooth in an accident, the extraction and treatment fall under accident coverage. If your cat develops a tooth root abscess from periodontal disease (an illness), the extraction typically receives coverage. But a routine cleaning to prevent future problems? That's wellness care and won't be covered unless you have a wellness rider.

Common Vet Procedures: Coverage at a Glance

| Procedure | Typical Coverage Status | Notes |

| Emergency visit fee | Covered | Subject to deductible and reimbursement level |

| ACL/cruciate ligament surgery | Covered after orthopedic waiting period | Usually requires 6-12 month waiting period |

| Cancer treatment (chemo/radiation) | Covered | Includes diagnostics, treatment, and medications |

| Routine dental cleaning | Excluded | Covered only with wellness add-on |

| Dental extraction (disease/injury) | Covered | When medically necessary, not preventive |

| Spay/neuter | Excluded | Covered only with wellness add-on |

| Diagnostic bloodwork (illness) | Covered | When investigating symptoms or monitoring disease |

| X-rays and imaging | Covered | For accidents and illnesses |

| Chronic medication (ongoing) | Covered | As long as condition isn't pre-existing |

| Behavioral therapy/training | Usually excluded | Some plans offer limited coverage |

| Alternative therapies (acupuncture, rehab) | Depends on plan | Increasingly available as add-on or included benefit |

Emergency visit fees deserve special mention. Most veterinary emergency clinics charge $100-$250 just for walking through the door, before any treatment begins. Some pet insurance policies cover this exam fee; others exclude it even when they cover the subsequent treatment. Check your policy's fine print.

Physical therapy and rehabilitation have gained coverage in recent years. If your dog needs hydrotherapy after orthopedic surgery or your cat requires physical therapy following a spinal injury, many modern policies now include these treatments. Alternative therapies like acupuncture and chiropractic care appear in some comprehensive plans, though coverage limits may apply.

Author: Ashley Reynolds;

Source: lamadone.net

Pre-Existing Conditions and Waiting Periods: The Fine Print That Matters

Pre-existing conditions represent the single biggest source of claim denials. Insurance companies define a pre-existing condition as any injury, illness, or symptom that existed, occurred, or showed clinical signs before your coverage started or during a waiting period.

Here's the tricky part: your pet doesn't need a formal diagnosis for something to count as pre-existing. If your dog limped before you bought insurance, and later that limping is diagnosed as hip dysplasia, the condition is pre-existing even though it wasn't diagnosed until after coverage began. Insurers review your pet's complete medical history when processing claims.

Some companies apply a "curable" pre-existing condition rule. If your cat had a urinary tract infection that was diagnosed, treated, and fully resolved before you purchased insurance, and then develops a completely new UTI a year later, some insurers will cover the new episode if your cat has been symptom-free for 180 days or more. Policies vary significantly on this point.

Waiting periods create additional coverage gaps:

- Accident waiting periods: 2-3 days after enrollment

- Illness waiting periods: 14 days after enrollment

- Orthopedic waiting periods: 6-12 months after enrollment for conditions like hip dysplasia, ACL tears, and patellar luxation

- Cruciate ligament waiting periods: Some insurers impose 12-month waits specifically for cruciate ligament injuries due to their frequency

Bilateral condition exclusions catch many pet owners off guard. If your dog tears the ACL in their left knee before coverage begins (making it pre-existing), some insurers will also exclude future tears in the right knee, arguing that bilateral conditions affecting matching body parts stem from the same underlying predisposition.

Most pet owners don't realize that even minor symptoms noted in medical records can disqualify coverage for related conditions later. I've seen claims denied for ear infections because the pet had a different ear infection years earlier, or allergies excluded because the owner mentioned itching during a routine visit.

— Dr. Sarah Mitchell, DVM

Breed-Specific and Hereditary Conditions: Coverage Limitations to Know

Hereditary and congenital conditions affect certain breeds disproportionately, and coverage varies by insurer. Hereditary conditions are genetic disorders passed from parents to offspring, like hip dysplasia in German Shepherds or heart disease in Cavalier King Charles Spaniels. Congenital conditions are present at birth, whether genetic or not, such as cleft palates or heart defects.

Most modern pet insurance policies cover hereditary conditions as long as symptoms first appear after coverage begins and waiting periods have passed. This represents a significant improvement over older policies that excluded hereditary conditions entirely.

However, the age at which you enroll your pet matters enormously. Hip dysplasia in large-breed dogs often shows symptoms between 6-18 months of age. If you wait until your Labrador Retriever is two years old to buy insurance, any hip problems that developed earlier—even if undiagnosed—become pre-existing.

Common breed-specific conditions and typical coverage scenarios:

- Hip dysplasia (German Shepherds, Golden Retrievers, Rottweilers): Covered if symptoms appear after the orthopedic waiting period; excluded if any limping, stiffness, or reluctance to exercise was noted before coverage

- Brachycephalic airway syndrome (Bulldogs, Pugs, French Bulldogs): Often covered, but some insurers exclude respiratory issues in flat-faced breeds entirely

- Heart conditions (Cavalier King Charles Spaniels, Dobermans, Boxers): Covered if diagnosed after coverage begins; some policies exclude specific cardiac conditions in high-risk breeds

- Eye conditions (Cocker Spaniels, Siberian Huskies, Poodles): Progressive retinal atrophy, cataracts, and glaucoma typically covered unless symptoms existed before enrollment

- Luxating patellas (small breeds like Chihuahuas, Yorkshire Terriers): Subject to orthopedic waiting periods; bilateral exclusions common

Enrolling your pet young—ideally before their first birthday—maximizes your chances of securing coverage for breed-related conditions before symptoms emerge.

Author: Ashley Reynolds;

Source: lamadone.net

How Reimbursement Levels and Annual Limits Affect Your Actual Coverage

Understanding what procedures your policy covers only tells half the story. The reimbursement structure determines how much you actually get back when you file a claim.

Reimbursement percentage represents the portion of covered expenses your insurer pays after you meet your deductible. Most plans offer choices of 70%, 80%, or 90% reimbursement. Higher percentages mean higher monthly premiums but lower out-of-pocket costs when you file claims.

Deductibles come in two forms: annual and per-incident. An annual deductible (typically $100-$1,000) applies once per policy year, after which your reimbursement percentage kicks in for all covered claims. A per-incident deductible applies separately to each new condition, which can become expensive if your pet develops multiple unrelated issues.

Annual limits cap how much your insurer will pay per policy year. Common limits include $5,000, $10,000, $20,000, or unlimited. Unlimited plans cost more monthly but protect you if your pet faces catastrophic illness requiring $30,000+ in treatment.

Here's a real calculation example:

Your dog needs ACL surgery costing $4,500. You have a $250 annual deductible (already met earlier this year), 80% reimbursement, and a $10,000 annual limit.

- Total bill: $4,500

- Deductible: $0 (already met)

- Insurance pays: $4,500 × 80% = $3,600

- You pay: $900

Now consider the same surgery with a $500 annual deductible (not yet met), 70% reimbursement, and a $5,000 annual limit:

- Total bill: $4,500

- Deductible: $500

- Remaining eligible expenses: $4,000

- Insurance pays: $4,000 × 70% = $2,800

- You pay: $1,700

That $800 difference in out-of-pocket costs stems entirely from policy structure, not coverage itself. When comparing plans, calculate potential costs for realistic scenarios your breed might face.

Some policies also impose per-incident limits (like $5,000 maximum per condition) or lifetime limits (total amount the insurer will pay over your pet's life). These restrictions can leave you underinsured if your pet develops an expensive chronic condition requiring ongoing treatment.

FAQ: Your Pet Insurance Coverage Questions Answered

Making Coverage Work for Your Pet's Needs

Pet insurance delivers the most value when you understand exactly what you're buying before your pet gets sick or injured. The difference between "we cover that" and "sorry, that's excluded" often hinges on timing, policy structure, and those pre-existing condition clauses buried in the fine print.

Enroll your pet young and healthy to avoid pre-existing condition exclusions for breed-specific issues that commonly develop later. Read your policy documents thoroughly—not just the marketing materials—and note specific exclusions, waiting periods, and reimbursement terms. Consider your breed's common health problems when choosing annual limits and reimbursement levels.

Calculate realistic scenarios based on your pet's breed, age, and lifestyle. If you own a Labrador Retriever, run the numbers on ACL surgery and cancer treatment. If you have a Bulldog, price out respiratory surgery and skin condition treatments. Match your coverage to actual risks rather than buying the cheapest policy available.

Pet insurance isn't a warranty that covers everything—it's financial protection against unexpected, expensive medical care. When chosen carefully and understood completely, it transforms a potential $10,000 emergency into a manageable $1,500 expense, letting you make medical decisions based on what's best for your pet rather than what you can afford in the moment.