From vet bill to reimbursement.

How Pet Insurance Reimbursement Works for Veterinary Bills

Content

Pet insurance reimbursement is the process by which your insurance company pays you back for covered veterinary expenses after you've already paid the vet bill out of pocket. Unlike human health insurance, where providers often bill your insurer directly, the vast majority of pet insurance policies in the United States operate on a reimbursement model.

Here's what that means for you: when your dog needs emergency surgery or your cat requires diagnostic imaging, you'll pay the veterinary clinic in full at the time of service. Afterward, you submit a claim to your insurance company, which reviews it and sends you a check or direct deposit for the covered portion of those expenses.

This model exists because the pet insurance industry is relatively young compared to human health insurance, and the infrastructure for direct billing simply isn't as developed. Veterinary clinics don't have the administrative capacity to navigate dozens of different insurance companies, each with unique policies and approval processes. The reimbursement approach keeps costs down for insurers and simplifies billing for veterinary practices, but it does mean pet owners need to have funds available upfront.

Understanding how reimbursement works before you face a veterinary emergency can prevent unpleasant surprises. The difference between what you pay and what you get back depends on several factors: your deductible, your chosen reimbursement percentage, annual limits, and whether your insurer uses actual cost or benefit schedule calculations.

The Pet Insurance Reimbursement Process: Step-by-Step

Paying Your Vet Bill Upfront

When you bring your pet in for treatment, the veterinary clinic will provide care and generate an itemized invoice. You're responsible for paying this bill before leaving, just as you would without insurance. Most clinics accept credit cards, debit cards, and sometimes payment plans through third-party financing companies like CareCredit or Scratchpay.

Keep every piece of documentation. Request an itemized invoice that lists each service, medication, and procedure separately. Many insurers won't accept a simple total—they need to see what they're reimbursing. Also ask for your pet's medical records related to the visit, including診斷 notes, test results, and treatment plans.

Submitting Your Claim (Documents You'll Need)

Most pet insurance companies offer multiple claim submission methods: online portals, mobile apps, email, or traditional mail. The digital options are fastest and let you track claim status in real time.

You'll typically need:

- A completed claim form (available through your insurer's website or app)

- An itemized invoice from your veterinarian showing each charge

- Medical records documenting the diagnosis and treatment

- Your policy number and pet's information

Some insurers have partnerships with veterinary software systems that allow clinics to submit claims directly on your behalf, though you still pay upfront. If your vet participates in one of these programs, they can often submit everything electronically while you're checking out.

Take photos or scan documents before submitting. If something gets lost in processing, you'll have backup copies. Missing or illegible paperwork is one of the most common reasons for claim delays.

Author: Megan Thornton;

Source: lamadone.net

How Long Does Reimbursement Take?

Processing times vary by company, but most insurers reimburse claims within 5 to 14 business days after receiving complete documentation. Some of the newer, tech-focused companies advertise reimbursement in as little as 2-3 days for straightforward claims.

Complicated cases involving pre-existing condition reviews, high-dollar amounts, or incomplete paperwork can take longer—sometimes 30 days or more. If your insurer needs additional information from your vet, they'll reach out, which adds time to the process.

You can usually choose between direct deposit and paper check. Direct deposit is faster, often shaving 3-5 days off the timeline since there's no mail transit time.

Understanding Reimbursement Percentages and How They Affect Your Payout

When you purchase a pet insurance policy, you select a reimbursement percentage—typically 70%, 80%, or 90%, though some insurers offer other options like 100%. This percentage determines what portion of covered expenses the insurer pays after you've met your deductible.

Higher reimbursement percentages mean you get more money back per claim, but they also increase your monthly premium. A policy with 90% reimbursement might cost 20-30% more per month than the same policy at 70% reimbursement.

The math is straightforward: if you have a $1,000 vet bill and a $250 annual deductible that you've already met, your 80% reimbursement policy would pay you $800 (80% of $1,000), leaving you with a $200 out-of-pocket expense. At 70%, you'd receive $700 and pay $300 yourself. At 90%, you'd get $900 and pay $100.

Here's how different reimbursement percentages affect your payout for the same veterinary bill:

| Reimbursement Level | Vet Bill Total | Deductible | Eligible Amount | Insurer Pays | You Pay (Total) |

| 70% | $1,000 | $250 | $750 | $525 | $475 |

| 80% | $1,000 | $250 | $750 | $600 | $400 |

| 90% | $1,000 | $250 | $750 | $675 | $325 |

Notice that the deductible comes off first, then the reimbursement percentage applies to what remains. Your total out-of-pocket cost includes both the deductible and your percentage share.

According to Dr. Sarah Chen, a veterinary practice consultant with 15 years of experience advising pet owners on insurance decisions: "The biggest mistake I see is people choosing the lowest reimbursement percentage to save on premiums, then being shocked when they're responsible for 30% of a $5,000 emergency surgery. Run the numbers on what you could realistically afford to pay out of pocket for a major incident, not just routine care."

Choosing your reimbursement percentage involves balancing monthly costs against potential emergency expenses. If you have savings set aside for pet emergencies, a 70% plan with lower premiums might work well. If a $2,000 unexpected bill would strain your budget, paying more monthly for 90% reimbursement provides better protection.

How Pet Insurance Calculates Your Reimbursement (With Real Examples)

The Role of Deductibles in Your Reimbursement

Your deductible is the amount you must pay before insurance coverage kicks in. Pet insurance deductibles typically range from $100 to $1,000, with $250 and $500 being most common. Lower deductibles mean higher premiums, but you'll reach coverage faster.

The deductible is always subtracted from your eligible expenses before the reimbursement percentage is applied. This is different from a copay, which would be calculated after reimbursement.

Annual vs. Per-Incident Deductibles

Annual deductibles reset once per policy year. You pay your deductible amount once, and after that, all covered claims for the rest of the year are reimbursed at your selected percentage without additional deductible charges. This structure works well if your pet has multiple health issues throughout the year.

Per-incident deductibles apply to each new condition or injury separately. If your dog tears an ACL in March and develops an ear infection in July, you'd pay the deductible twice—once for each unrelated condition. However, ongoing treatment for the same condition typically doesn't require paying the deductible again.

Most pet owners find annual deductibles more predictable and cost-effective, especially for pets with chronic conditions requiring ongoing care.

Author: Megan Thornton;

Source: lamadone.net

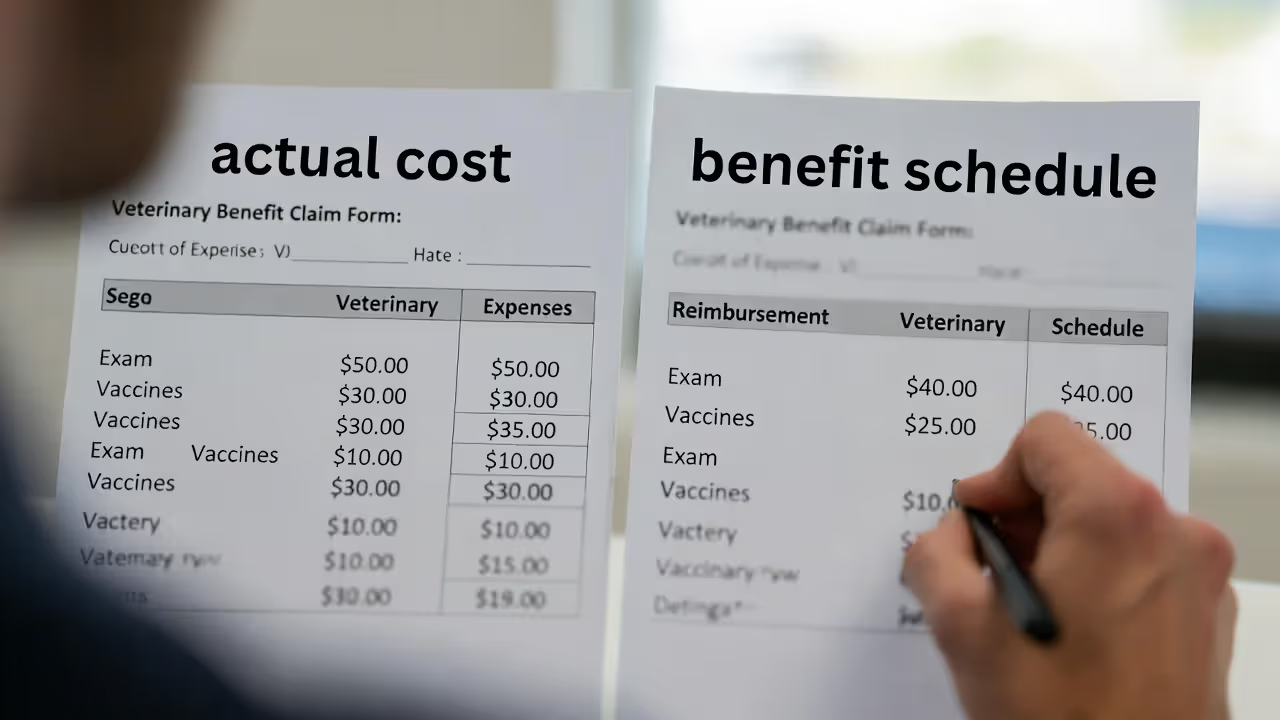

Actual Cost vs. Benefit Schedule Reimbursement

Most modern pet insurance policies use actual cost reimbursement, meaning they reimburse based on what your vet actually charged. If your vet bills $800 for a procedure, that's what the insurer uses for calculations (minus deductible and percentage).

Some older policies or budget plans use benefit schedules, which set predetermined maximum amounts for specific procedures regardless of what your vet charges. If the schedule allows $500 for a dental cleaning but your vet charges $800, you'll only be reimbursed based on $500, even with 90% coverage. These policies are generally less favorable for pet owners, especially in high-cost areas where veterinary prices exceed schedule amounts.

Always verify which reimbursement method your policy uses. Actual cost policies provide more comprehensive protection.

Example 1: Routine Procedure ($500 ear infection treatment)

- Vet bill: $500

- Annual deductible (already met): $0 remaining

- Reimbursement percentage: 80%

- Calculation: $500 × 80% = $400

- You receive: $400

- Your cost: $100

Example 2: Emergency Surgery ($3,000 foreign body removal)

- Vet bill: $3,000

- Annual deductible: $250 (not yet met this year)

- Reimbursement percentage: 90%

- Calculation: ($3,000 - $250) × 90% = $2,475

- You receive: $2,475

- Your cost: $525 (deductible + 10% of remaining amount)

Example 3: Same Surgery, Different Terms

- Vet bill: $3,000

- Per-incident deductible: $500

- Reimbursement percentage: 70%

- Calculation: ($3,000 - $500) × 70% = $1,750

- You receive: $1,750

- Your cost: $1,250

These examples show how significantly your policy terms affect your actual reimbursement. The difference between scenarios 2 and 3 is $725—nearly 25% of the total bill.

Common Reimbursement Policy Restrictions You Should Know

Author: Megan Thornton;

Source: lamadone.net

Even with comprehensive coverage, certain limitations affect what you'll actually get reimbursed. Understanding these restrictions prevents frustration when filing claims.

Waiting periods prevent you from filing claims immediately after purchasing coverage. Most policies have 14-day waiting periods for illnesses and 6-month waiting periods for orthopedic conditions like cruciate ligament tears or hip dysplasia. Accidents typically have shorter waiting periods, often just 2-3 days. Any treatment needed during waiting periods won't be reimbursed.

Pre-existing conditions are never covered. If your pet showed symptoms of a condition before your coverage started, or during a waiting period, that condition is excluded permanently. This includes chronic issues like diabetes, allergies, or arthritis that were diagnosed or treated before enrollment.

Annual limits cap how much your insurer will reimburse per policy year. Common limits are $5,000, $10,000, or unlimited. Once you hit your annual limit, you're responsible for 100% of additional costs until the policy renews. Unlimited plans cost more but provide the best protection against catastrophic expenses.

Per-incident limits cap reimbursement for each individual condition. A policy might have a $5,000 per-incident limit, meaning if your pet's cancer treatment costs $15,000, you'd only receive $5,000 total for that condition, regardless of your annual limit.

Certain procedures are commonly excluded from coverage: breeding costs, cosmetic procedures, elective surgeries, preventive care (unless you purchase a wellness add-on), and pre-existing conditions. Some policies also exclude specific hereditary or congenital conditions, particularly in certain breeds.

Exam fees are sometimes excluded or limited. Some insurers don't reimburse for the veterinary examination itself, only for diagnostics and treatment. Others include exam fees but cap reimbursement at $50-100 per visit.

Pet insurance reimbursement works best when owners understand the math before an emergency happens. Knowing how deductibles and reimbursement percentages affect the final payout helps avoid unpleasant surprises when the vet bill arrives.

— Dr. Amanda Lewis, Veterinary Insurance Advisor

5 Mistakes That Delay or Reduce Your Reimbursement

- Submitting incomplete paperwork. Missing signatures, unclear photos of invoices, or forgetting to include medical records forces insurers to request additional information, adding weeks to processing time. Double-check that every required field is completed and all documents are legible before submitting.

- Filing claims for excluded services. Submitting claims for preventive care when you only have accident and illness coverage, or filing for a pre-existing condition, wastes your time and creates a paper trail that might complicate future claims. Read your policy documents to understand what's actually covered.

- Missing claim deadlines. Most insurers require claims within 90 days to one year of the date of service. File promptly after treatment—waiting until you've accumulated several vet visits might push early visits past the deadline.

- Not understanding your annual limit. If you've already received $8,000 in reimbursements and your policy has a $10,000 annual limit, you only have $2,000 coverage remaining for the year. Submitting a $4,000 claim won't get you $4,000 back—you'll receive $2,000 and be responsible for the rest.

- Choosing the wrong reimbursement method at signup. Some insurers let you select your reimbursement percentage when you enroll, but changing it later requires waiting periods or isn't allowed at all. Carefully consider what percentage makes sense for your financial situation before purchasing, not after you've filed your first big claim.

Frequently Asked Questions About Pet Insurance Reimbursement

Pet insurance reimbursement doesn't need to be confusing once you understand the basic mechanics: you pay upfront, submit documentation, and receive a percentage of covered expenses back after your deductible is met. The key to maximizing your reimbursement is choosing policy terms that match your financial situation—balancing monthly premiums against potential out-of-pocket costs during emergencies.

Before purchasing coverage, calculate what you'd actually pay for realistic scenarios. A $3,000 emergency surgery with a $250 deductible and 90% reimbursement leaves you with $525 out of pocket, while 70% reimbursement means paying $1,075. That $550 difference might be worth the higher monthly premium if your budget can't absorb larger unexpected expenses.

Keep detailed records, submit claims promptly with complete documentation, and understand your policy's specific restrictions around waiting periods, annual limits, and excluded conditions. The reimbursement process becomes routine once you've filed a few claims, and having coverage in place provides genuine financial protection when your pet needs expensive veterinary care.